On Hormuz (and concretely leveraging geography)

I spent an evening going down a macro rabbit hole after reading Citrini Research’s field report on the Strait of Hormuz. One of their analysts was physically on the water near Oman, watching tankers transit through Iran’s checkpoint system, talking to fishermen and shipping captains. So sick. I texted some thoughts I’d had about it to my friend Cameron the next morning and our subsequence conversation sharpened a few of these ideas considerably. This post came out of that exchange.

I went in expecting to learn about oil prices and trade baskets. I came away thinking about energy and geography. For thirty-odd years the assumption has been that where you sit on the map is subordinate to economics and US naval hegemony. Open seas, free trade, plug into the global system and your coordinates don’t matter much. I think Hormuz is showing us that assumption was wrong – and the investment baskets, the proxy wars, the ceasefire negotiations all make more sense when you look at them through that lens. This isn’t a new argument – Kaplan’s Revenge of Geography made the case in 2012, Zeihan’s been running the demographic/geographic thesis for a decade. What feels novel is watching the mechanism work in real time – Iran didn’t just leverage geography abstractly; they built a literal toll booth. The ships are transiting now, under a dozen flags, negotiating with geography directly. That’s what this post is about.

But first, the baskets

Citrini published three trade baskets around the Middle East disruption. A “trade basket” is basically a curated list of stocks that express a thesis – if you believe X is going to happen, buy these companies. The percentages next to each name tell you how much of your money goes into each one.

If you’re a finance person and already grokked all the necessary info on this stuff from the original post, feel free to skip this section, but as someone not super long on this stuff, I found that these baskets were a useful framework for the non Bloomberg terminal-pilled. Each one captures a different theory about how geopolitical chaos flows through markets.

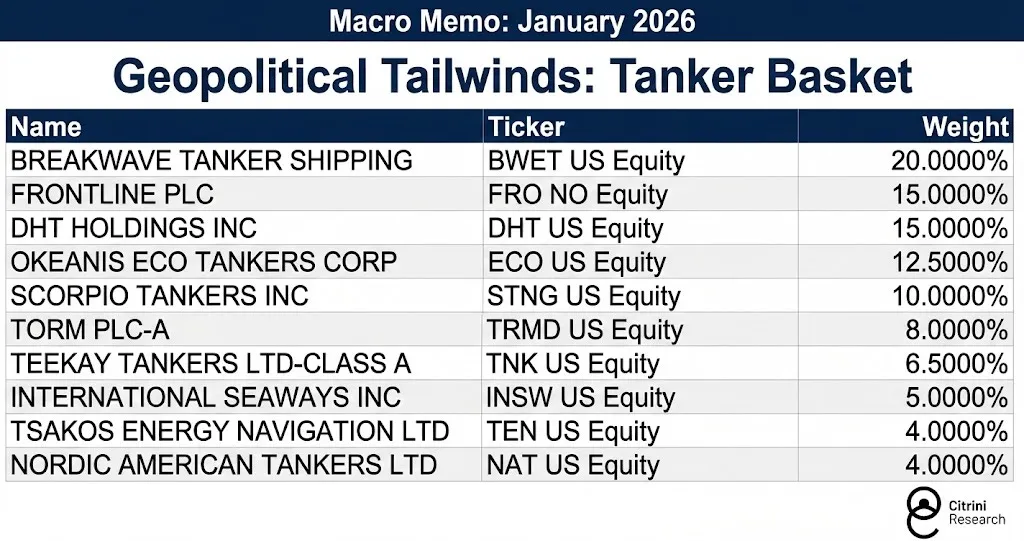

Tanker basket. These are companies that own and operate the massive ships that move crude oil around the world. Frontline, DHT, Scorpio, a bunch of others. The biggest position is BWET, an ETF that tracks tanker freight futures – essentially a direct bet on shipping rates going up. When shipping lanes get dangerous, ships reroute around Africa instead of through Suez. Same oil, way more ships needed, way more days at sea. Rates spike. BWET has quadrupled since Citrini first recommended it.

Energy/commodities basket. Broader oil supply chain: companies that drill, refine, run pipelines, make fertilizer (natural gas is the main input for fertilizer, so energy disruption hits them hard). Oil went from $67 on February 27 to around $118 at peak. This basket is a straightforward “disruption means higher energy prices” bet. Citrini’s highest conviction play here is actually US petrochemicals – Dow and Westlake – because Gulf infrastructure damage will take 250-275 days to repair even after Hormuz reopens. US producers sitting on cheap domestic feedstock benefit regardless of how the conflict resolves.

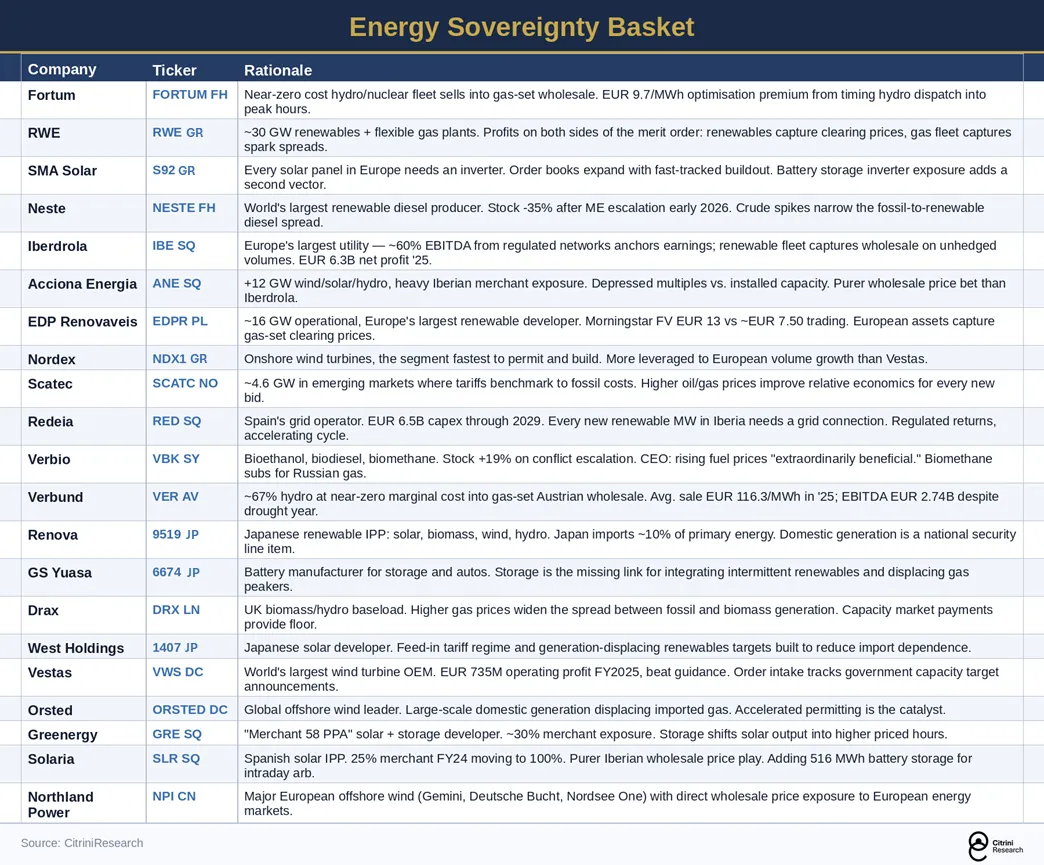

Energy sovereignty basket. This one’s different. It’s almost entirely European and Japanese renewables companies – Vestas, Orsted, Iberdrola, RWE, plus grid infrastructure and solar hardware manufacturers. The bet is that every government watching Hormuz close now has political mandate to fast-track domestic energy buildout. Permits, subsidies, grid investment. The utilities in this basket (Fortum, Verbund, Acciona) have a particularly elegant setup: they own renewable assets with near-zero marginal cost but sell into wholesale electricity markets where the price is set by gas. When gas prices spike, their margins explode even though their costs didn’t change. Slower burn than the other two baskets, less volatile, probably only up modestly so far. But arguably the most durable thesis.

The ceasefire announced yesterday hammered all three baskets, at least short term.

The toll booth

The detail from Citrini’s field report that stuck with me most is that Iran hasn’t actually closed the strait. They’ve set up a checkpoint system through the Qeshm-Larak channel. Ship owners submit vessel details – ownership, flag, cargo, crew – to brokers. Payments go through cash, crypto, or diplomatic arrangements. Approved vessels get escorted through Iranian waters. The analyst observed at least 15 ships crossing on April 2, up from 2-5 daily in prior weeks. Ships flying Indian, Malaysian, Japanese, Greek, French, Chinese, Turkish, and Omani flags. All transiting independently. Without Washington’s approval.

Iran has turned a chokepoint into a toll booth. The Strait of Hormuz is 21 miles wide at its narrowest point, 20% of global oil transits through it1, and Iran sits on the northern shore. That’s leverage you can’t sanction away and can’t replicate somewhere else. And the place you can see the old order breaking down most clearly is in who’s transiting right now and how they’re doing it – independently, on their own terms, without asking Washington.

Cameron framed the broader picture well: Iran and Ukraine are the pre-WWI/II proxy fights, the ones where the major powers try to settle the new order without going at it directly. You can already see it in the mediation patterns. Pakistan popping up as a “surprise” mediator in the US-Iran talks makes a lot more sense when you realize China sent them.

Geography starts to matter

Cameron and I’s conversation covered a lot of ground, but three regions kept coming up – each one illustrating a different way that physical location is reasserting itself over financial abstraction.

Iran. If sanctions get dropped as part of the ceasefire framework, 1.5-2 million barrels per day of suppressed supply re-enter the market. That’s an oil price story, sure. But Iran has been selling heavily discounted crude to China and India through shadow fleets for years because they have no other buyers. Sanctions gone means normal banking, normal pricing, normal trade relationships. Give Iran access to SWIFT and suddenly Beijing isn’t the only trading partner worth having. The toll booth at Hormuz gave Iran leverage; sanctions relief would give them options.

Cuba. Alfred Thayer Mahan called Cuba “the key to the Gulf of Mexico” the same way Gibraltar is the key to the Mediterranean2, and looking at a map you can see why. Cuba flanks both the Yucatan Channel (connecting the Gulf to the Caribbean) and the Straits of Florida (connecting the Gulf to the Atlantic). Any vessel entering or leaving the Gulf passes within range of Cuban shores. That includes the shipping lanes carrying roughly 13% of total US crude oil production from Gulf platforms to refineries and markets.3

This matters right now because Russia and China are actively building presence there. In June 2024, Russian warships carrying hypersonic missiles docked in Havana – the largest Russian show of force with Cuba in years.4 Russia ratified a formal military cooperation agreement with Cuba in October 2025.5 Meanwhile, CSIS has identified four Chinese signals intelligence facilities on the island through satellite imagery, including one at Bejucal less than 100 miles from Florida that can monitor Kennedy Space Center launches.6 In March 2026, a Russian oil tanker broke the US fuel blockade with 100,000 tonnes of crude.7

In short: Cuba caps the Gulf for the US and gets Russia out of our hemisphere. That’s a Monroe Doctrine argument. The economics of Cuba – nearshoring, tourism, whatever – are hypothetical and frankly unrealistic under current conditions. Trump is running maximum pressure, the island’s population has dropped over 10% in four years from emigration8, the power grid collapsed in March.9 None of that changes where Cuba is on a map. It controls chokepoints the same way Iran does, and other powers are already treating it accordingly.

The EU. The EU-as-superpower scenario is probably the most underpriced thing in markets right now. Common defense spending, real industrial policy, joint debt issuance – if it happens you get a completely different European investment surface. But the reason it’s underpriced is because it’s genuinely hard. The Franco-German engine that’s supposed to drive consolidation is stalled: their EUR 100B+ joint fighter jet program (FCAS) is collapsing over workshare disputes10, Macron is pushing for common EU debt and Germany is explicitly rejecting it11, and their competing visions for industrial policy are pulling other member states into opposing camps.

The energy picture is a useful reality check. Europe has spent EUR 300 billion on REPowerEU12, cut Russian gas imports from 45% to 13%13, tripled US LNG imports13, and hit a milestone in 2025 where wind and solar generated more EU electricity than fossil fuels for the first time.14 And despite all that, the Hormuz closure – which directly affects only about 10% of EU LNG15 – still sent Dutch gas benchmarks nearly doubling, triggered fuel rationing in Slovenia16, and forced the ECB to postpone rate cuts. Geography doesn’t care about your spending programs.

But I think the most interesting take on this whole geography thing has to do with trade routes and climate. Historically, European power flows East-West through the Mediterranean. Spain, Italy, Greece – they control the sea lanes, which makes them more strategically important within the EU than their GDP might suggest. But global warming means the Arctic is opening up. China already runs an “Arctic Express” container service from Shanghai to Rotterdam, Hamburg, Gdansk, and Felixstowe – 18 days versus 35-50 via Suez.17 Nature Communications projects the first ice-free Arctic day before 2030.18 As the northern passages become viable, the UK, the Netherlands, and Norway gain strategic weight as trade destinations – potentially at Mediterranean expense. (The Arctic angle probably deserves its own post, but it’s worth flagging here because it illustrates the same point from a different direction.)

Italy sees it coming – they’re counter-investing in Trieste as a rail gateway to Central Europe, trying to stay relevant in a world where ships might skip the Mediterranean entirely. The geography of Europe is pulling in two directions at once, and climate change is accelerating the split. That tension makes a unified EU bloc harder to achieve in ways that don’t show up in the usual federalist pitch.

Bits still need atoms

Here’s where I’ll bring it back to what I actually know something about: cloud software and AI.

The popular version of the AI story is that software is weightless, models run in the cloud, bits move at the speed of light. Geography fades into irrelevance. But the infrastructure underneath all of that is profoundly physical, and it’s getting more physical every year. Dylan Patel at SemiAnalysis estimates that the big four hyperscalers will deploy roughly 50 gigawatts of compute capacity this year, backed by around $600 billion in CapEx. Every one of those gigawatts needs power from a physical place. Google is buying energy companies. Hyperscalers are putting deposits down on turbines and locking in power purchasing agreements years in advance. The constraint on AI scaling is increasingly “where can you plug this in” – and that’s a geography question.

The supply chain is even more concentrated. ASML in the Netherlands makes roughly 70 EUV lithography machines per year – the tools you need to fabricate leading-edge AI chips. Patel calculates that you need about three and a half EUV tools per gigawatt of AI compute. That puts a hard ceiling on total global capacity: maybe 200 gigawatts by 2030, and that’s if everything goes right. TSMC in Taiwan fabricates the chips. Samsung and SK Hynix in South Korea make the high-bandwidth memory. The entire AI buildout runs through a handful of specific facilities in a handful of specific countries, several of which sit in the same part of the Pacific that’s become the other major theater of great power competition.

Every gigawatt of new compute deepens the dependency on specific places – where the power is, where the fabs are, where the lithography machines come from. AI only makes geography more important.

The ships transiting Hormuz under a dozen different flags aren’t waiting for a diplomatic resolution. They’re negotiating directly with geography. I suspect the next decade will be defined by who else figures that out.

-

U.S. Energy Information Administration, “The Strait of Hormuz is the world’s most important oil transit chokepoint.” ↩

-

Alfred Thayer Mahan, via USNI Proceedings, “Cuba’s Place in U.S. Naval Strategy” (December 1962). ↩

-

U.S. Energy Information Administration, “Gulf of America crude oil production forecast to remain near record highs in 2025 and 2026.” The Gulf produces ~1.8 million barrels/day, approximately 13% of total US crude production. ↩

-

PBS NewsHour, “Russian warships arrive in Cuban waters for military exercises” (June 2024). The frigate Admiral Gorshkov and nuclear submarine Kazan both carry Zircon hypersonic missiles. ↩

-

CiberCuba, “Russia Ratifies Military Alliance with Cuban Regime” (October 2025). Signed in Havana March 13, ratified by Russia’s parliament October 2025. ↩

-

CSIS, “China’s Intelligence Footprint in Cuba” (July 2024 and December 2024). Four facilities identified via satellite imagery at Bejucal, Wajay, Calabazar, and El Salao. ↩

-

Wikipedia, “2026 Cuban crisis.” Russian oil tanker delivered 100,000 tonnes of crude to Havana on March 30, 2026. ↩

-

CiberCuba, “Cuban Emigration 2025” (December 2025). Over 860,000 Cubans arrived in the US alone between 2021 and mid-2024; population fell from ~11.2 million to 9.7 million. ↩

-

Wikipedia, “2026 Cuban crisis.” Cuba’s entire power grid collapsed on March 16, 2026, following the cutoff of Venezuelan and Mexican oil supplies. ↩

-

Euronews, “Is Europe’s mega defence project FCAS in danger of failing?” (November 2025). Dassault demanded 80% workshare; Germany warned parliament this was unacceptable. ↩

-

Euronews, “Macron pushes for EU common debt capacity” (February 2026). Germany and Italy jointly circulated a counter-document to EU capitals opposing Macron’s position. ↩

-

European Commission, “REPowerEU.” EUR 300 billion total mobilized (EUR 72B grants, EUR 225B loans), with EUR 113 billion allocated for renewables and hydrogen through 2030. ↩

-

EU Council, “Where does the EU’s gas come from?” Russian gas dropped from 45% of EU imports (2021) to 13% (2025). US LNG now accounts for 56% of EU LNG imports. ↩ ↩2

-

Ember, “Wind and solar generated more power than fossil fuels in the EU for the first time in 2025.” ↩

-

IEEFA, “Strait of Hormuz disruption would jeopardise 10% of Europe’s LNG imports.” ↩

-

TIME, “Strait of Hormuz: How the crisis is driving energy rationing.” (April 2026). Slovenia introduced fuel rationing; Austria implemented fuel tax cuts and retailer profit caps. ↩

-

High North News, “China launches 18-day Arctic Express containership route to Europe.” Operated by Haijie Shipping with stops at Felixstowe, Rotterdam, Hamburg, and Gdansk. ↩

-

Nature Communications, “First ice-free Arctic day possible before 2030” (2024). Most models converge around ~2034 for consistently ice-free September conditions. ↩